If you’ve ever opened a credit card or savings account, you’ve probably seen the terms APR and APY. They look similar — but they mean very different things.

Understanding the difference can save you thousands of dollars over time.

Let’s break it down in the simplest way possible.

📌 What Is APR?

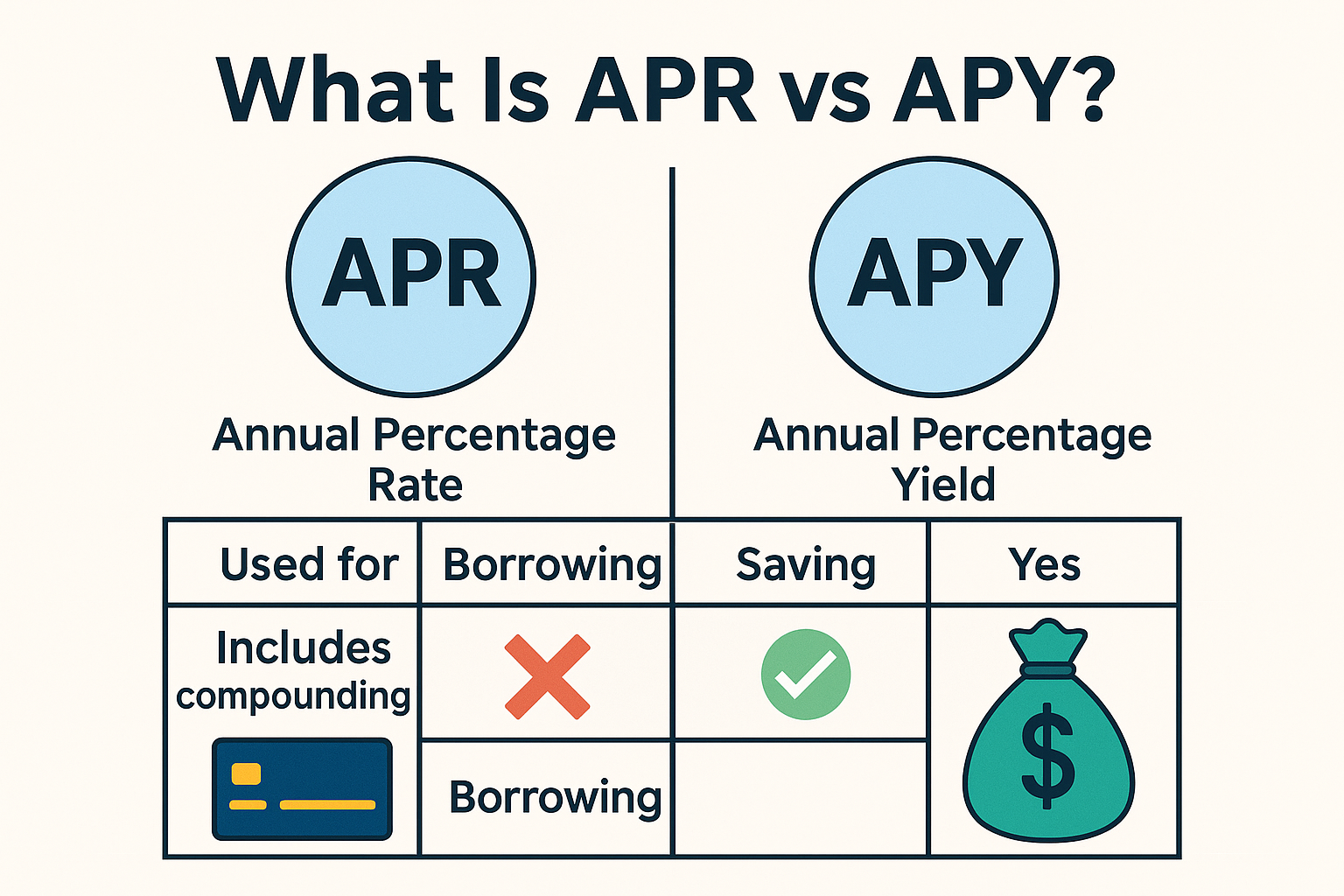

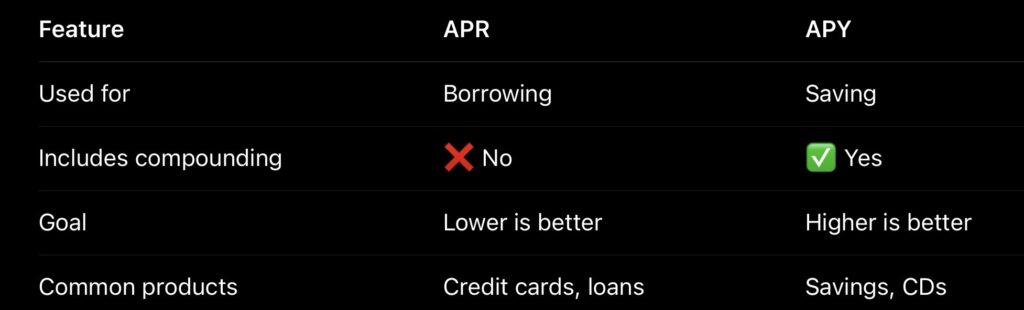

APR (Annual Percentage Rate) represents the yearly cost of borrowing money.

It’s commonly used for:

Credit cards Personal loans Auto loans Mortgages

🔹 Key points about APR:

Shows how much interest you pay per year Does not include compound interest Lower APR = cheaper debt

👉 Example:

If a credit card has a 20% APR, you’re paying roughly 20% per year on your balance.

📌 What Is APY?

APY (Annual Percentage Yield) represents how much interest you earn on savings or investments including compound interest.

It’s used for:

Savings accounts High-yield savings CDs Money market accounts

🔹 Key points about APY:

Includes compound interest Higher APY = more money earned Compounding can be daily, monthly, or yearly

👉 Example:

A savings account with 4.5% APY earns more than 4.5% simple interest because of compounding.

⚔️ APR vs APY: What’s the Difference?

💡 Why This Difference Matters

If you:

Borrow money → focus on APR Save or invest → focus on APY

Many people lose money simply because they don’t understand this distinction.

📈 Real-Life Example

Credit card: 22% APR → expensive debt Savings account: 4.8% APY → money grows passively

Using high-APY accounts while avoiding high-APR debt is one of the smartest financial moves you can make.

🧠 Final Thoughts

APR tells you how much debt costs.

APY tells you how much your money earns.

Knowing the difference helps you:

Choose better financial products Avoid unnecessary debt Grow your savings faster

Financial literacy starts with small concepts like this — and they make a huge difference long-term.